What Is Reverse Budgeting

Reverse budgeting is an innovative and strategic approach to managing finances, which places a higher emphasis on saving and investing, even before considering the monthly expenses. This stands in stark contrast to the conventional methods of budgeting, where one typically deducts their monthly expenses from their income, and whatever remains is saved.

In the traditional budgeting approach, saving is often a residual activity, carried out with whatever funds are left after all expenses have been accounted for. However, reverse budgeting turns this concept on its head by encouraging individuals to prioritize savings first, and then allocate the remaining funds to cater to their monthly expenses.

This methodology might strike a chord with business owners, specifically those operating small businesses. This is due to the fact that reverse budgeting shares a similar principle with a common approach used in small businesses known as 'Profit First' by Mike Michalowicz.

Much like how the Profit First methodology prioritizes profit, reverse budgeting prioritizes savings. Both of these methods encourage the practice of setting aside a portion of the income first (profit in businesses, and savings for individuals), before addressing expenses. This strategy promotes financial stability and growth, both in personal and business domains.

- How To Implement Reverse Budgeting

- Benefits Of Reverse Budgeting

- Drawbacks Of Reverse Budgeting

- Final Thoughts

How To Implement Reverse Budgeting

Here's how to put reverse budgeting into practice:

1. Identify Your Goals

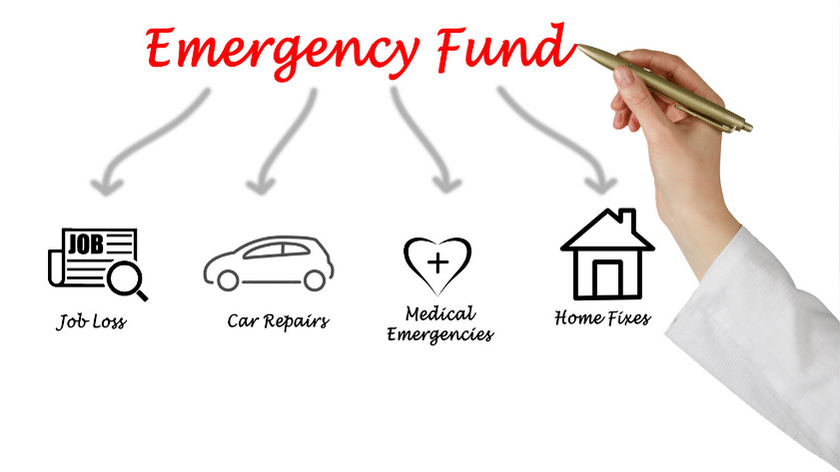

Begin by identifying your financial goals, which can vary widely depending on your personal circumstances and future plans. These could include saving for retirement, which is a long-term goal that requires consistent and disciplined saving over years, if not decades. If home ownership is a dream of yours, setting a goal to save for a down payment on a house could be another objective. It's important to note that this can be a substantial amount, so early and planned saving is crucial. An emergency fund is another important financial goal, which serves as a safety net for unexpected expenses such as medical emergencies, unexpected job loss, or any unforeseen financial crisis. You might also have other individual financial goals depending on your lifestyle, ambitions, and commitments, such as saving for a child's education, a dream vacation, or for starting a business. Identifying these goals clearly is the first step towards effective reverse budgeting.

2. Calculate Your Required Savings

Start with a clear understanding of your financial objectives. These could be short-term goals such as saving for a vacation or long-term targets like retirement. Based on these goals, calculate the total amount you need to accrue. Then, divide this total by the number of months until your goal's deadline. This will give you the amount you need to save each month. Remember, it's crucial to be realistic when setting your savings target. It should be a figure that's challenging to reach, but not so high that it's impossible or puts you under severe financial strain. If necessary, adjust your timeframe or goal amount until you find a balance that's ambitious yet achievable.

3. Deduct Savings Goal From Monthly Income

After determining your monthly savings target, the next step in reverse budgeting involves deducting this amount from your total monthly income. This is a deliberate move to ensure that your savings are accounted for right at the beginning, rather than at the end of the month after all expenses have been met. By subtracting your savings goal from your income first, you are essentially paying yourself first. This helps to reinforce the concept of saving as a priority, rather than as an afterthought. It encourages a mindset of living within your means after savings have been factored in, rather than saving what is left over after expenses. This step requires discipline and commitment, but it's a crucial part of the reverse budgeting process that can significantly contribute to achieving your long-term financial goals.

4. Allocate Remainder Towards Monthly Expenses

Once you've set aside your savings from your total monthly income, the next step in reverse budgeting is to allocate the remaining income to your monthly expenses. These expenses may encompass a variety of categories depending on your lifestyle and necessities. Major categories often include housing, represented by rent or mortgage payments, and utilities, such as electricity, gas, water, and internet services. These are generally fixed expenses that occur on a regular basis and are essential for maintaining your standard of living.

In addition, you'll need to budget for groceries, which can vary month by month based on dietary preferences, the size of your household, and any specific dietary needs. Other necessary expenses might include transportation costs, whether that's fuel for a car, public transit fares, or maintenance for a bicycle. You may also need to account for insurance payments, such as health, car, or home insurance, and any regular debt repayments like student loans or credit card bills.

It's important to remember that these expenses can fluctuate, so it's beneficial to track them over several months to get an accurate estimate for budgeting purposes. By carefully allocating your income to cover these expenses, after prioritizing savings, you can ensure that your financial needs are met without sacrificing your long-term financial goals. This approach requires a thorough understanding of your spending habits and a commitment to living within your means, but it can significantly contribute to achieving financial stability and growth.

5. Discretionary Spending

Any remaining income after accounting for savings and necessary expenses can be allocated towards discretionary spending. This category includes non-essential purchases that often contribute to your quality of life and personal enjoyment. Examples of discretionary spending could include entertainment options like movie tickets, subscriptions to music or streaming services, dining out at restaurants, or even splurging on a weekend getaway.

Discretionary spending also provides an opportunity for personal hobbies and interests. This could involve buying a new book, investing in fitness equipment, or purchasing materials for a craft project. It's the area of your budget that gives you the freedom to spend on things that make you happy and enrich your life.

However, it's crucial to remember that this is the last step in the reverse budgeting process. It should only be considered after you've achieved your savings goals and covered all essential expenses. This way, you can enjoy your discretionary spending guilt-free, knowing that you've responsibly managed your financial priorities.

By treating discretionary spending as a reward rather than a given, you're more likely to appreciate these purchases and experiences. This approach can also help you to make more mindful spending decisions, as you'll be consciously choosing to spend money on the things you truly value.

Benefits Of Reverse Budgeting

Reverse budgeting offers a multitude of benefits that can significantly enhance financial management and growth. Key among these is its focus on prioritizing saving and investing. Instead of treating savings as an afterthought, this approach places them at the forefront of financial planning. This ensures consistent and regular contributions towards your financial goals, helping you make significant strides over time.

Another major advantage of reverse budgeting is its ability to curb overspending. By allocating funds to savings first, you're left with a clear picture of what remains for monthly expenses. This can prevent the tendency to spend beyond one's means and promotes a healthier and more manageable financial lifestyle.

More importantly, reverse budgeting encourages a more mindful approach to spending. Rather than impulsively spending on wants and desires, this budgeting method prompts individuals to think twice about their expenditures. Discretionary spending is treated as a reward that comes after meeting financial obligations, not as a given. This fosters a greater appreciation for these purchases and experiences, leading to more thoughtful spending decisions.

Furthermore, reverse budgeting brings financial stability and growth not just in personal finance but also in the business domain. Similar to the 'Profit First' approach used by businesses, prioritizing savings first ensures a steady cushion for future growth and unexpected setbacks. It adds a layer of financial security that can prove invaluable in times of uncertainty.

One of the standout features of reverse budgeting is its flexibility. It doesn't prescribe a rigid formula, but rather offers a framework that can be tailored to your unique financial circumstances and goals. Whether you're saving for a down payment on a house, building an emergency fund, or setting aside money for retirement, reverse budgeting can be adjusted to accommodate these objectives.

This approach to budgeting is proactive, placing you in the driver's seat of your financial future. It shifts the focus from simply tracking and categorizing expenses to actively planning and prioritizing your financial goals. This hands-on approach to managing money fosters a greater sense of control and ownership over your finances.

In summary, reverse budgeting is a transformative approach to managing finances. It molds the act of saving from a residual to a priority, encourages more mindful spending habits, averts overspending, and fosters financial stability and growth. Its flexibility allows it to be tailored to individual financial situations and goals, making it a reliable and effective tool for anyone looking to gain control over their financial future.

Drawbacks Of Reverse Budgeting

While reverse budgeting offers numerous advantages, it also presents potential challenges that might make it less suitable for certain individuals. One of such challenges is its suitability for those with inconsistent income or unpredictable expenses. Those who rely on a fluctuating income, such as freelancers, entrepreneurs, or seasonal workers, might find it difficult to set a fixed savings goal each month. Similarly, individuals with unpredictable or variable expenses might struggle to accurately calculate how much they can afford to save without risking a shortfall.

Another potential drawback pertains to the level of financial discipline and self-control required. Reverse budgeting fundamentally prioritizes savings, and this could present a temptation to tap into these savings for non-essential or discretionary purchases. The success of this budgeting method hinges on the ability to resist such temptations and consistently prioritize savings. This could prove challenging for individuals who are not used to such a structured approach to managing their money or those who have not yet developed strong financial discipline.

Additionally, for people burdened with high levels of debt, the strategy of prioritizing savings might not be the most effective or beneficial. The reason being, the interest accrued on outstanding debt could potentially outweigh the benefits derived from savings or investment returns. In such cases, a more aggressive debt repayment plan could prove to be a more financially sound strategy.

Finally, while reverse budgeting is a powerful tool for financial planning, it might not fully account for unexpected expenses. Unexpected expenses, whether they are related to health emergencies, sudden home repairs, or unplanned travel, could disrupt the carefully balanced equation of saving and spending. Therefore, those using reverse budgeting should also consider building an emergency fund to cater to such unanticipated expenses.

In conclusion, while reverse budgeting is a transformative approach to personal finance and can significantly enhance savings and investments, it does come with potential drawbacks. These challenges underline the importance of adapting and customizing budgeting strategies to align with personal income levels, financial discipline, debt situations, and the possibility of unexpected expenses. It's crucial to understand these potential challenges and adapt the method to ensure it best serves your unique financial needs and circumstances.

Final Thoughts

While reverse budgeting fundamentally advocates for the prioritization of savings and investment, it is important to clarify that this does not necessitate a complete disregard for personal wants or pleasures. Rather, the main principle underpinning reverse budgeting is that your key financial objectives should be addressed first, with the remaining money then allocated responsibly for personal desires and needs. This approach is advantageous as it not only instills a sense of financial discipline, helping to prevent unnecessary debt, but also allows for a certain degree of personal enjoyment and satisfaction from your hard-earned money.

In essence, reverse budgeting doesn't mean you have to forego your lifestyle or comforts. Instead, it emphasizes a structured approach to spending - where saving isn't an afterthought, but a priority. It's about creating a balance between today's needs and tomorrow's dreams, between financial responsibility and personal happiness. It's about enjoying your money, guilt-free, knowing you have prioritized and taken care of your financial future.

Moreover, the flexibility inherent in reverse budgeting allows for its integration with other budgeting strategies, potentially leading to a more personalized and effective approach to money management. For example, one popular strategy is The 50/30/20 Rule, which suggests that 50% of your income should be allocated to essential needs, 30% to personal wants, and the remaining 20% to savings. You could apply the principles of reverse budgeting to this last part, ensuring that your savings are not just an afterthought, but a priority. By doing so, you are creating a well-rounded financial plan that ensures both your current comfort and future security.

This combination of budgeting strategies can offer a balanced and comprehensive approach to manage your finances. It addresses the different aspects of your financial life - needs, wants, and savings. It ensures that you are saving for the future, meeting your current needs, and also enjoying your life today. By creating such a balance, you are more likely to stick to your budget, achieve your financial goals, and enjoy a financially secure life.

At its core, reverse budgeting is a highly adaptable strategy that can be molded to fit your specific financial conditions and objectives. It provides a proactive framework for money management, placing you firmly in the driver's seat of your financial journey. Rather than being reactive to financial circumstances, you become proactive, planning, and managing your finances in a way that best suits you. It's not just about managing money, but about managing your financial future. With reverse budgeting, you gain control, you become empowered to shape your financial future according to your goals, needs, and dreams.

Looking for more tips to help you achieve your goals? Check out: